Looking to estimate your Pinellas County property tax for 2026? Understanding how your local property taxes are calculated can save you money, help you plan your annual housing budget, and prevent any surprises when your official tax bill arrives.

From the Just Value determined by the Property Appraiser to local millage rates and exemptions like Homestead, Florida follows a specific multi-step formula. With changing real estate values and updated local levies, Pinellas County homeowners need precise calculations to manage their finances effectively. Discover how the property tax system works and learn how to plan ahead today.

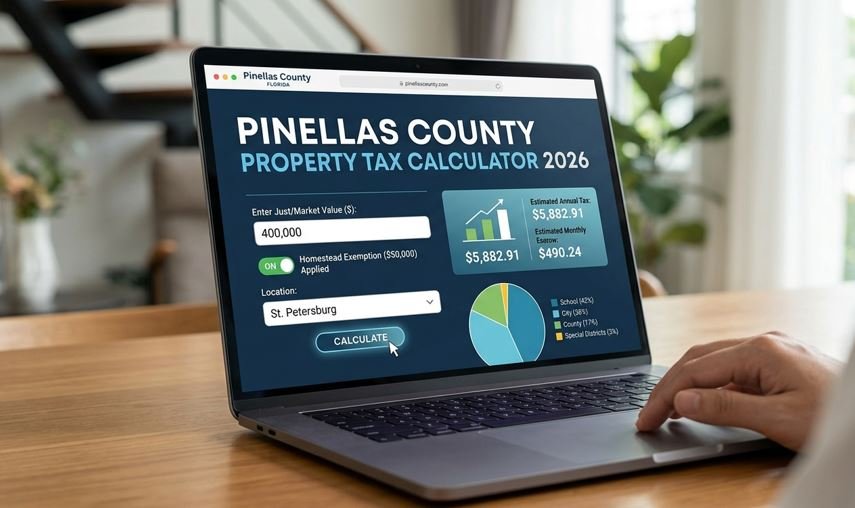

Pinellas County 2026 Property Tax Estimator

Estimate your property tax based on local representative millage rates and standard Florida exemptions.

Disclaimer: This is an informational estimate based on representative millage rates. Actual certified tax amounts may vary based on exact parcel locations and final county assessments.

Pinellas County Property Tax Breakdown (2026 Proposed)

Unlike some states that use flat percentages, Florida property tax relies on Millage Rates set by local taxing authorities (County, City, School Board, and Water Management Districts). A millage rate is the amount of tax payable per $1,000 of a property’s taxable value.

The table below shows an illustrative example breakdown for a typical residential property in Pinellas County with an Assessed Value of $400,000 and a standard $50,000 Homestead Exemption:

| Taxing Authority | Representative Millage Rate (per $1,000) | Estimated Annual Tax Amount | Percentage of Total Tax |

| Pinellas County Operating | 4.7398 mills | $1,658.93 | ~36.8% |

| School Board (Local & State) | 5.4320 mills | $1,901.20 | ~42.2% |

| City / Municipal Levy (e.g., St. Petersburg) | 6.4250 mills | $2,248.75 | Varies by City |

| Water Management & Special Districts | 0.2115 mills | $74.03 | ~1.6% |

| Total Estimated Tax | 16.8083 mills | $5,882.91 / year | 100% |

Important Note on Homestead Exemption: The School Board levy only applies the first $25,000 of the Homestead Exemption, while City and County levies apply the full $50,000 exemption. This is why the taxable value differs across components.

How to Calculate Your Pinellas County Property Tax

Calculating your property tax involves a structured procedural workflow. If you want to run a manual check or verify your official notice, follow these essential steps:

1.Find Your Just/Market Value:Step 1.

Locate your property’s Just Value (Market Value) using the Pinellas County Property Appraiser’s official database. This value is established as of January 1st of the tax year.

2.Apply the Save Our Homes (SOH) Cap:Step 2.

If the property is your primary residence and has a Homestead Exemption, ensure the Save Our Homes assessment cap is applied. This limits annual assessment increases to 3% or the Consumer Price Index (whichever is lower), giving you your Assessed Value.

3.Deduct Eligible Exemptions:Step 3.

Subtract your exemptions from the Assessed Value to find your Taxable Value. For primary homeowners, subtract the standard $50,000 Homestead Exemption (noting the $25,000 variance for school taxes).

4.Multiply by Total Millage Rate:Step 4.

Divide your Taxable Value by 1,000 and multiply it by the combined millage rate of your specific city, school district, and county zone.

$$\text{Property Tax} = \left( \frac{\text{Taxable Value}}{1000} \right) \times \text{Millage Rate}$$

Key Terms You Need to Know

To audit or estimate your tax correctly, make sure you do not confuse these values:

- Just Value: The actual market value of your property as estimated by the county appraiser.

- Assessed Value: The value of the property after applying any assessment caps or limitations (like Save Our Homes).

- Taxable Value: The final value used to calculate your dollar tax amount after subtracting all exemptions.

Tips for Accurate Estimates & Lowering Your Bill

- File for Homestead Exemption: If you moved to Pinellas County recently, ensure you apply for the Homestead Exemption before the March 1st deadline to secure your tax caps and deductions.

- Check for Additional Exemptions: Pinellas County offers additional property tax relief for seniors with limited income, disabled veterans, widows/widowers, and visually impaired individuals.

- Review Your TRIM Notice: Every August, the county sends out the Truth in Millage (TRIM) notice. Review this document carefully; it outlines the proposed rates and gives you a window to appeal your property assessment if you believe it is overvalued.

Conclusion

Estimating your Pinellas County property tax in 2026 doesn’t have to be a complicated process. By leveraging the step-by-step calculation workflow and understanding how the standard Florida $50,000 Homestead Exemption divides across school and county levies, homeowners can structure their annual finances with absolute precision.

While using an online calculator provides an instant, clear snapshot for monthly mortgage allocation and escrow budgeting, always remember that these numbers are structured around representative millage rates. For final certified tax statements, official valuation appeals, or critical assessment updates, always consult the official Pinellas County Property Appraiser (PCPAO) and Tax Collector portals. Planning your property expenses ahead of time is the best way to safeguard your real estate investments and avoid year-end escrow shortages.

FAQS

What is the average property tax rate in Pinellas County?

The effective property tax rate in Pinellas County typically averages between 1.3% to 1.6% of the property’s assessed value, depending highly on the specific municipality or city you reside in.

When are Pinellas County property taxes due?

Property tax bills are mailed out in November. Taxes are due by March 31st of the following year. However, early payment discounts are available: 4% off in November, 3% in December, 2% in January, and 1% in February.

How does a tax estimator tool help with budgeting?

An online estimator breaks down your combined rates into monthly mortgage allocations, helping you structure your escrow accounts accurately and avoid year-end shortages.